Sectors we work in

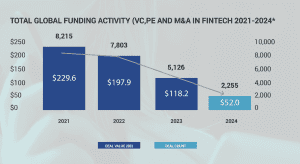

Global fintech funding has experienced a rollercoaster ride since 2020 and securing

investment has become increasingly challenging, with funding at a four year low in H1 2024.

High interest rates, ongoing geopolitical uncertainty and increased regulatory scrutiny mean that fintechs are increasingly required to demonstrate strong financial performance, innovative products, and scalable business models.

Total global funding (VC, PE and M&A) was at $52B H1 2024, whilst deal count for H1 was 2255 deals. There was a decline from the previous year across all funding activity types, the biggest decline was in PE, with a value of $1B vs $9.6 for 2023 (whole year).

Despite such muted market conditions, the latest Future of Fintech Report from Silicon Valley Bank (SVB) found some cause for optimism. They note that Venture Capital deal flow has shifted towards early stage, with more than three seed deals for every series A. The report also sees potential in significant growth in AI as investors and founders explore its increasingly significant role.

The payments sector remained dominant in global fintech investment, and showing

growth, with $22.4B in the first half of 2024, vs $22.7B in the whole of 2023. These figures are slightly distorted, however, by megadeals for Worldpay and Nuvei – $18.8B collectively. Without these, the sector is subdued.

Deal volume was low – 231 behind even 2023 which saw a 6 year low on deal volumes.

KPMG do envisage a potential uptick in activity towards the end of 2024, which is already becoming evident following the US election.

Blockchain/cryptocurrency saw stabilisation in H1 2024 with value of $3.2B globally, following a significant drop in both deal volume and value in 2023 ($8.5B vs $22.3B in 2022). Deals were smaller, with only 5 over $100M, but deal volume remained good – 677 H1 2024 vs 1268 in the whole of 2023. KPMG noted that during H1 2024, lines between tradfi and de-fi began to blur. “In the US, traditional financial instruments — such as bonds and treasury bills — were tokenised and brought into the de-fi world, while crypto assets were wrapped in traditional financial infrastructure to improve investor confidence and enhance investment opportunities”.

The US market was characterised by regulation in H1 2024, whilst EMEA and Asia

Pacific were focused on development and launch of digital currencies. The impact of the Republican US election victory and resultant political conditions enabling development in this area is already apparent with the price of Bitcoin reaching an all time high of $97,000 on 21st November.

H1 2024 saw insuretech funding fall to its lowest level in a decade ($1.6B), less than a quarter of the $8,2B in the whole of 2023. The cost of capital and a focus on AI enablement continued to restrict investment in insuretech, and M&A activity was low, except for the purchase of Corvus by Travellers.

In contrast regtech performance strengthened in H1 2024 – $5.3B value from 134 deals vs $3.4B, 284 deals in the whole of 2023. Leonard Green’s $4B buyout of IRIS Software bolstered the sector, but more generally there is increasing interest in regtech from both VC and PE investors.

Whilst cybersecurity saw a quiet H1 2024 with $640M investment vs $1.4B in the whole of 2023, volume remained strong, with 40 deals in H1, leaving the sector on track to match or better deal volume in 2023 (71 whole year). AI continued to be a key area of interest and investment in H1’ 2024, with investors focusing on a range of AI applications, from AI-driven risk intelligence platforms to AI powered supply chain security solutions.

A similar picture is emerging in wealthtech, with investors showing interest in how AI can play a role in enhancing wealth management. Wealthtech investment levels are low at $100M and 18 deals, but on a par with 2023 activity ($0.2M, 37 deals whole year). There was continued interest in ESG-related wealth management products and solutions from individual investors, particularly high net worth individuals looking to make ESG investments, which could be a platform for growth of the wealthtech sector.

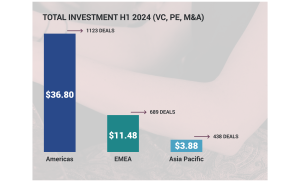

Innovate Finance’s H1 2024 Fintech Investment Landscape report saw the US leading global fintech VC investment with a 46% market share, in line with recent years, followed by the UK with 12.7% and India with 5%. In terms of total (VS, PE, M&A) investment, the Americas achieved $36B, EMEA $11.4B and Asia Pacific $3.6B. UK accounted for $7.3B of the EMEA total. Total deal volumes H1 2024 were 1123 in the Americas, 689 EMEA (UK 198) and 438 Asia Pacific.

The Americas saw a persistent valuation gap in VC and PE areas, which coupled with the high interest rate, kept VC and PE investment subdued during H1 2024. There is a growing interest in taking public fintechs back to private, driven by the early IPO activity in 2021 and 2022 followed by challenging market conditions. The Nuvei deal, taken private by Advent for $6.2B in H1 2024, is the largest of these deals.

Fintech investment in the Americas fell slightly — from $38.5B in H2 2023 to $36.7B in H1 2024, but with a rise in deal volume from 1,066 to 1,123. The US lead total global fintech investment in H1 2024 with c46% (?) market share at $27.4B. The high interest-rate environment, geopolitical uncertainty, and lingering valuations challenges are thought to account for the decrease in larger deals.

KPMG’ Pulse of Fintech H1 2024 report notes a growing interest in taking fintechs private. 2021 and 2022, saw significant fintech IPO activity in the fintech space, including a number going public via SPAC mergers. Since that time, a number of these companies have struggled given the challenging market environment, leading to growing interest in taking companies that went public early, private again. During H1’24, the largest of these take-private deals was Nuvei by Advent International for $6.3B.

Dealmaking looks to be evening out to levels similar to 2023 – total funding deals in H1 2024 were 1123 vs 2374 in the whole year in 2023. Overall volumes look to be flattening out to historical averages when the highs of 2021/22 are excluded.

KPMG highlighted the following emerging trends: consolidation in the payments space, particularly niche fintechs being acquired by more mature fintechs looking to grow and scale; regulators increasing attention on issues like data protection and privacy, particularly in the US; wealthtech investments focusing more on B2B support fintechs rather than on B2C businesses; growing focus on AI enablement, not only in the regtech space, but in the insurtech sector as a means for assessing risks.

Buyout of Worldpay – $12.5B

Public to Private Buyout EngageSmart – $4B

M&A Tegus – $930M

Series B Clear Street – $685M

M&A Cadre – $500M

EMEA showed resilience in VC investment ($5.4B) compared to other regions in H1 2024, which along with more interest in early-stage deals has led to optimism over the IPO market reopening in H2 2024. B2B focussed fintechs were of particular interest to investors, whilst in the UK, a number of mature fintechs have looked to international expansion to drive growth with mixed results. Starling Bank and Oak North are selling tech internationally as banking SaaS platform plays.

Innovate Finance’s research shows a UK decline in funding in line with the global landscape. There is an expectation that equity funding will remain challenging with onerous terms around exit and use of proceeds. White and Case predict an increasing willingness in fintech to accept alternative debt solutions or credit lines from banks.

198 UK M&A, PE and VC fintech deals completed in H1 2024, down from 284 in H1

2023.

UK saw the largest fintech focused VC deal of H1’24—a $999 million raise by Abound.

Total UK fintech investment hit $7.3 billion in the first half of 2024, up from $2.5 billion in the same period in 2023 (KPMG’s latest Pulse of Fintech Aug ’24 report) VC investment accounted for $2B in H1 2024.

UK outperformed wider EMEA region. EMEA dropped $7.7B to $11.4B in H1 2024

Geopolitical uncertainty, high levels of inflation and the high-interest rate environment have all contributed to more subdued levels of UK fintech investment, compared to the record highs experienced in 2021/22

The Fintech Impact Report 2024 scored the UK fintech market at an overall net impact score of 24 (in a spectrum -100 to +100) for ESG/impact, higher than capital markets, construction and retail sectors.

Buyout of IRIS Software by Leonard Greed – $4B

Debt and equity round for Abound – $1.1B

Monzo fund raising – $610M

Asia Pacific – despite a slight uptick in deal volume over the same period (406 to 438), total investment in Asia Pacific declined from $4.6B in H2 2023 to $3.7B in H1 2024. M&A and PE investments were particularly soft in the region during H1’24, with M&A accounting for just $300 million in deal value and PE accounting for just $7.8 million.

None of the 10 biggest global fintech deals were outside EMEA and the Americas, the largest Asian Pacific deals included $280M raised by China’s Yi’an Enterprise, $209M by Indian KreditBee and $195M by Thai based Ascend.

AI has continued to be an area of focus in the region with fintechs enhancing AI components of their solutions and offerings.

Whilst China’s Five Finance central government strategy continues to work with financial institutes to encourage start ups in digital, pension, green, inclusive and tech finance, investment in H1 24 declined to $624M, from $754.6 in H2 23, and both quarters were muted compared to historical trends.

The ASEAN group of countries, however, does appear to show resilience. PWC Fintech in ASEAN 2024 Report notes that as global fintech funding is facing a third consecutive year of decline, ASEAN has held steady – 1% decline YOY vs 35% decline in funding in North America and Europe, and a 12% decline in APAC excluding ASEAN.

Seed and early-stage investments account for c60% of total fintech funding in the region, boosted by two mega deals – GuildFi and Longbridge. These deals suggest that

investors may be willing to bet on foundation level innovation, based on future returns

The backing also suggests ASEAN as an incubator for new fintech ideas, a good indicator of long-term health.

The share of investments into late-stage firms declined as a cautious economic environment hampered exit opportunities.

Average deal size increased by 8 per per cent year-on-year from US$13.8 million to US$14.2 million in 2024. Furthermore, the Federal Reserve’s interest rate cut in September is expected to potentially revive venture capital interest Singapore and Thailand accounted for three quarters of the total fintech funding in the region in 2024. Singapore also has the highest number of fintech unicorns in ASEAN.

Indonesia, dropped to third this year, lacking mega deals and a reduction in its funding share of the funding pie with no mega deals. Thailand was propped by Ascend Money’s US$195 million mega deal. Philippines are sitting at fourth, driven by Uno

Bank’s US$32 million deal.

GuildFi – US$140m

Longbridge – US$100m

Ascend Money – $195m

Uno Bank – $32m

“Early assessment suggests that H2 2024 followed similar patterns to H1 2024.

2025 will bring both challenge and opportunity to financial services and to fintech in particular. The new year has been characterised by the US trade tariffs and responses which are continuing to play out and the impact is too early to assess.

Changing consumer behaviour in recent years, combined with technological disruption and global economic and geopolitical uncertainty means that traditional and established institution will be increasingly in competition with challenger banks and fintech disruptors, whilst navigating AI and changing customer expectations”.

In addition to the impact of tariffs, we expect 2025 trends to include:

Advances in AI in the back office

AI regulation, oversight and transparency

Focus on cyber preparedness

Central Bank digital currencies

Race for tech talent

20 North Audley Street,

Mayfair

London

W1K 6WE

Yorkshire House

Greek Street

Leeds

LS1 5SH